Domestic Bills Of Exchange

Description

This section is from the book "Elementary Economics", by Charles Manfred Thompson. Also available from Amazon: Elementary Economics.

Domestic Bills Of Exchange

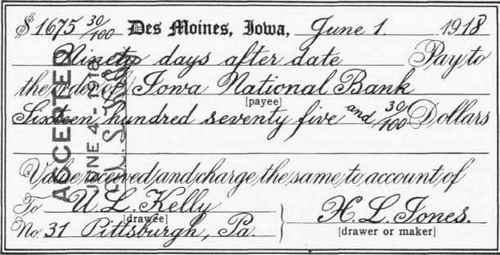

Some sellers resort to a third method to collect from their debtors - a domestic bill of exchange. Let us suppose that a corn-buyer in Iowa has an order for a carload of corn from a cattle-feeder in Pennsylvania. As soon as he has loaded the car he gets from the railroad company a bill of lading which specifies among other things the amount of corn in the car, the name of the consignor (shipper) and the name of the consignee. He then draws a draft (domestic bill of exchange) on the consignee in which he orders him to pay at sight or at the end of some stipulated period, such as sixty days, the purchase price of the corn. Now the shipper is ready to visit his banker. He presents the draft and the bill of lading to the bank, which credits his account with the amount named in the draft. There are now three parties known in the transaction, the drawer (shipper of the corn), the drawee (buyer of the corn), and the payee (banker). The Iowa bank now sends the draft with attached bill of lading to some bank in the neighborhood of the drawee. This bank presents the draft to the drawee, who either pays the amount named in it, if it is a sight draft, or if it is a time draft, he accepts it by writing across its face the word accepted. In any case the railroad bill of lading is turned over to him, for without it he cannot get possession of his carload of corn.

Domestic Bill of Exchange.

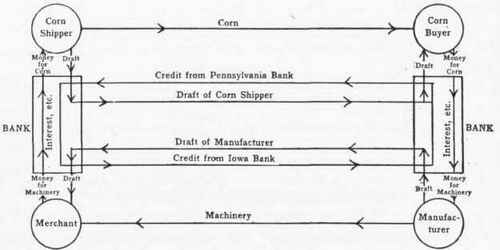

It is conceivable that a Pennsylvania manufacturer, a neighbor of the buyer of the corn, should sell several machines to a hardware merchant in the Iowa town where the shipper of the corn lives, and that he too should draw a draft on the merchant for the amount of his bill. If the two amounts were exactly the same and the same two banks handled both transactions, the two debts would be canceled without shipping money in either direction. If the amounts were not the same the difference between them would have to be settled in some other manner.

These various movements can be easily seen by examining the illustration (Fig. 8, page 247). Provided the two amounts of money involved were the same, the Iowa bank merely pays to the corn-shipper what it collects from the hardware merchant, while the Pennsylvania bank pays to the manufacturer what it collects from the buyer of corn. In both cases the banks charge, in addition to a nominal fee, interest for the use of their money.

Fig. 3.

Continue to:

My Books