8. Elasticity Of Demand. Nature Of An Elastic Demand

Description

This section is from the book "Elementary Economics", by Charles Manfred Thompson. Also available from Amazon: Elementary Economics.

8. Elasticity Of Demand. Nature Of An Elastic Demand

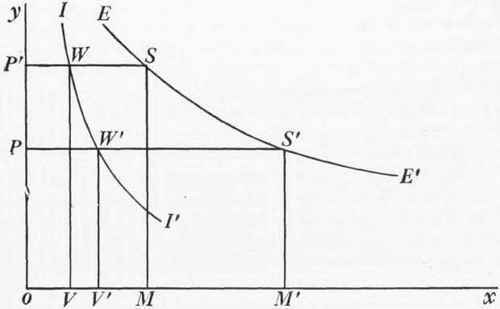

All demands are more or less elastic; that is, the demand for any particular good tends to increase as its price falls. In the case of some, the increase is very rapid, of others, very slow. Somewhere between these two extremes is an indeterminate boundary line separating elastic demand from inelastic demand. Elasticity of demand is, therefore, a relative term, since no demand is absolutely elastic or absolutely inelastic. Generally speaking, the demand for luxuries is elastic, for each slight decline in price tends to cause a relatively large increase in demand. Literally thousands of men were persuaded a few years ago to buy a certain make of automobile when the price was reduced but a little more than ten per cent. Conversely, a general increase in the prices of automobiles caused by the Great War had an immediate effect in curtailing demand; though in this particular case curtailment was not as great as it would have been had there not been a rise in the prices of practically all other goods. Curve EE' in Fig. 1 serves to illustrate the character of an elastic demand. A fall in price from OP' to OF (that is, from MS to M'S') causes an increase in the demand from OM to OM' (P'S to PS').

Fig. 1.

Continue to:

My Books